The introduction of the new tax regime under Section 115BAC of the Income Tax Act has provided taxpayers with an alternative to the old tax regime. This article provides a comprehensive comparison between the old and new tax regimes, detailing the various exemptions and deductions available, and illustrating the differences with a case study.

1. Overview of the Old and New Tax Regimes

Old Tax Regime

-

- Structure: The old tax regime offers lower tax rates and multiple exemptions and deductions.

-

- Flexibility: Taxpayers can reduce their taxable income through various deductions and exemptions.

-

- Complexity: Requires careful tax planning and documentation to maximize tax savings.

New Tax Regime (FY 2024-25)

-

- Structure: Introduced in FY 2020-21, offers reduced tax rates with no or limited exemptions and deductions.

- Simplicity: Designed to simplify the tax filing process with straightforward tax rates.

- Choice: Taxpayers can choose annually between the old and new regimes.

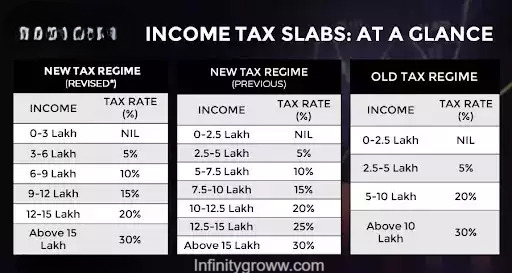

2. Tax Rates Comparison

Old Tax Regime (FY 2024-25)

- Up to ₹2.5 lakh: Nil

- ₹2.5 lakh to ₹5 lakh: 5%

- ₹5 lakh to ₹10 lakh: 20%

- Above ₹10 lakh: 30%

New Tax Regime (FY 2024-25)

- Up to ₹3 lakh: Nil

- ₹3 lakh to ₹6 lakh: 5%

- ₹6 lakh to ₹9 lakh: 10%

- ₹9 lakh to ₹12 lakh: 15%

- ₹12 lakh to ₹15 lakh: 20%

- Above ₹15 lakh: 25%

3. Key Exemptions and Deductions in the Old Tax Regime

- Section 80C: Investments and Expenses

-

- Maximum Deduction: ₹1,50,000

- Eligible Investments/Expenses: Life Insurance Premium, Public Provident Fund (PPF), Employee Provident Fund (EPF), National Savings Certificates (NSC), 5-year fixed deposits, tuition fees, principal repayment of home loan, Equity Linked Savings Scheme (ELSS).

- Section 80CCC: Pension Funds

- Maximum Deduction: ₹1,50,000 (combined limit with 80C and 80CCD)

- Eligible Investments: Contributions to annuity plans of LIC or other insurers.

- Section 80CCD: National Pension Scheme (NPS)

- Maximum Deduction:

- Employee’s contribution: ₹1,50,000 (combined limit with 80C and 80CCC).

- Additional deduction: ₹50,000 for NPS Tier I account contributions.

- Maximum Deduction:

- Section 80D: Health Insurance Premium

- Maximum Deduction:

- Self, spouse, and children: ₹25,000.

- Parents (less than 60 years old): ₹25,000.

- Parents (60 years old or above): ₹50,000.

- Additional deduction of ₹5,000 for preventive health check-up.

- Maximum Deduction:

- Section 80E: Education Loan Interest

- Eligible Deduction: Interest on education loan for higher studies (no upper limit on the amount).

- Section 80G: Donations to Charitable Institutions

- Eligible Deduction: Varies from 50% to 100% of the donation amount, subject to specific conditions and limits.

- Section 80GG: Rent Paid

- Maximum Deduction: ₹5,000 per month or 25% of total income or actual rent paid minus 10% of income, whichever is lower.

- Section 80TTA: Interest on Savings Account

- Maximum Deduction: ₹10,000 on interest income from savings accounts.

- Section 80TTB: Interest on Deposits for Senior Citizens

- Maximum Deduction: ₹50,000 on interest income from deposits with banks, post office, or cooperative banks (for senior citizens).

- Section 24(b): Home Loan Interest

- Maximum Deduction:

- Self-occupied property: ₹2,00,000.

- Let-out property: No limit on the interest deduction.

- Maximum Deduction:

- Section 10(14): Special Allowances

- Includes: Children Education Allowance, Hostel Allowance, Transport Allowance for disabled individuals.

- Section 10(10D): Life Insurance Payouts

- Tax-free if the premium paid in any year does not exceed 10% of the sum assured.

- Section 10(13A): House Rent Allowance (HRA)

- Deduction based on the least of the following:

- Actual HRA received.

- 50% of salary (for metro cities) or 40% (for non-metro cities).

- Rent paid minus 10% of salary.

- Deduction based on the least of the following:

- Section 10(1): Agricultural Income

- Agricultural income is exempt from tax, but it is considered for calculating the tax rate on non-agricultural income.

4. Key Features of the New Tax Regime

- Standard Deduction Increase: The standard deduction for salaried individuals has been raised from ₹50,000 to ₹75,000.

- Family Pension Deduction Increase: The maximum deduction for those receiving a family pension has been increased from ₹15,000 to ₹25,000.

- Employer’s Pension Contribution Deduction: The deduction for an employer’s contribution to a pension scheme under Section 80CCD (2) has been increased from 10% of the salary to 14% of the salary.

5. The Eligibility Criteria for the New Tax Regime under Section 115BAC

To opt for the new tax regime under Section 115BAC, taxpayers must meet the following eligibility criteria:

- Individual Taxpayers: Available to individuals, including both residents and non-residents.

- Hindu Undivided Families (HUFs): Available to HUFs.

- Annual Option: Taxpayers can choose between the old and new regimes each financial year.

- No Carry Forward: Losses from previous years cannot be carried forward if opting for the new regime.

6. Exemptions and Deductions Not Claimable under the New Tax Regime

Under the new tax regime, the following exemptions and deductions are not claimable:

- Section 80C: Investments in PPF, EPF, LIC, etc.

- Section 80D: Health insurance premiums.

- Section 80E: Interest on education loans.

- Section 80G: Donations to charitable institutions.

- House Rent Allowance (HRA): Exemption for HRA is not available.

- Leave Travel Allowance (LTA): Exemption for LTA is not available.

- Standard Deduction: Standard deduction of ₹50,000 is not available.

- Professional Tax: Deduction for professional tax is not available.

- Interest on Housing Loan: Deduction for interest on housing loan is not available.

7. Case Study: Taxpayer with ₹12 Lakh Annual Income

Scenario 1: Old Tax Regime

Income Details:

- Annual Income: ₹12,00,000

- Deductions:

- Section 80C (Investments): ₹1,50,000

- Section 80D (Health Insurance): ₹25,000

- Section 24(b) (Home Loan Interest): ₹2,00,000

- Total Deductions: ₹3,75,000

- Taxable Income: ₹12,00,000 – ₹3,75,000 = ₹8,25,000

Tax Calculation:

- Up to ₹2.5 lakh: Nil

- ₹2.5 lakh to ₹5 lakh: 5% of ₹2.5 lakh = ₹12,500

- ₹5 lakh to ₹8.25 lakh: 20% of ₹3.25 lakh = ₹65,000

Total Tax Payable: ₹12,500 + ₹65,000 = ₹77,500

Scenario 2: New Tax Regime

Income Details:

- Annual Income: ₹12,00,000

- No Deductions Applicable

Tax Calculation:

- Up to ₹3 lakh: Nil

- ₹3 lakh to ₹6 lakh: 5% of ₹3 lakh = ₹15,000

- ₹6 lakh to ₹9 lakh: 10% of ₹3 lakh = ₹30,000

- ₹9 lakh to ₹12 lakh: 15% of ₹3 lakh = ₹45,000

Total Tax Payable: ₹15,000 + ₹30,000 + ₹45,000 = ₹90,000

6. Conclusion

Choosing between the old and new tax regimes depends on an individual’s income, available deductions, and financial planning strategies. The old regime is beneficial for those who can claim significant exemptions and deductions, while the new regime simplifies the tax process with lower rates and minimal paperwork.